Consumer Bankruptcies, Foreclosures, Delinquencies, and Collections: Free Money Still Doing the Job

Powell mentioned lots of instances customers can choose tightening due to the fact loan distress is at historic lows. What buyers can not take for extensive is raging inflation.

By Wolf Richter for WOLF Avenue.

We’ll start out with customer bankruptcies due to the fact which is in which credit history troubles, if they can not be fixed, usually stop up. Then we’ll appear at foreclosures, 3rd-party collections, and delinquencies. What emerges is the photograph of a purchaser, even now flush with pandemic cash and soaring incomes.

Shopper bankruptcies had plunged when the totally free money arrived, like the PPP financial loans, together with the various forbearance courses and the eviction bans. And the number of buyers with bankruptcies ongoing to fall to historic lows and have been hobbling along all those historic lows for the very last 12 months-and-a-fifty percent.

In the 3rd quarter, the number of shoppers with bankruptcies inched up a tad from the 2nd quarter, to 99,000, but was continue to below a yr back, in accordance to facts from the New York Fed’s Household Debt and Credit score Report, and 50 {8ba6a1175a1c659bbdaa9a04b06717769bcea92c0fdf198d429188ebbca09471} of the currently reduced degrees of the Fantastic Moments (all over 200,000):

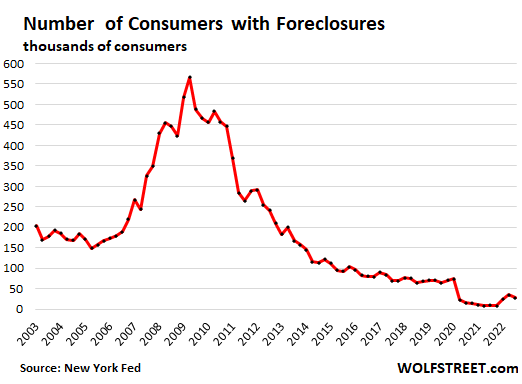

Foreclosures dipped in the 3rd quarter and have been at extremely-historic lows considering that the mortgage loan forbearance plans, exactly where delinquent home loans ended up put on ice, and no longer counted as delinquent. Most of the borrowers have now exited the forbearance packages, either by possessing the home loan modified in some way, or by obtaining bought the household and paid off the property finance loan, which was effortlessly probable amid the pandemic spike of household charges. The totally free pandemic revenue also served.

Foreclosures, right after ticking up for two quarters, ticked down once more in Q3 to just 28,500 home loans with foreclosures, thus nixing the beginnings of a craze that experienced been forming. For the duration of the Very good Situations right before the pandemic, there had been about 70,000 home loans with foreclosures, more than double the current selection:

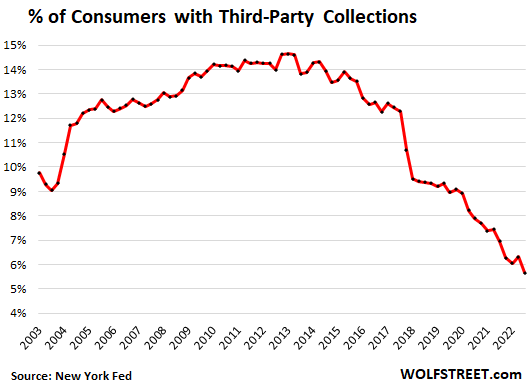

The part of Consumers with 3rd-social gathering collections dropped to a new historic very low in Q3, to just 5.7{8ba6a1175a1c659bbdaa9a04b06717769bcea92c0fdf198d429188ebbca09471}, right after a slight uptick in Q2. 3rd-social gathering collections are registered on a consumer’s credit report when a lender offered a severely delinquent account for cents on the dollar to a collection agency which will then hound the defaulter for some quantity greater than what it experienced paid out for:

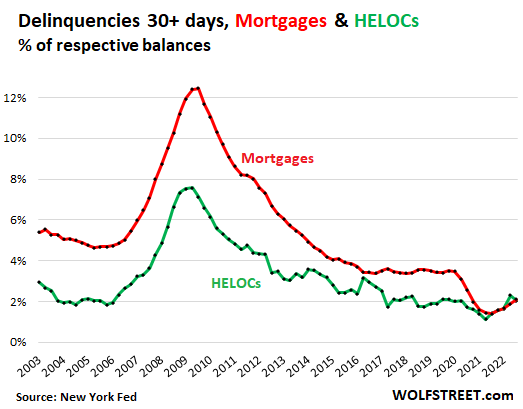

House loan and HELOC delinquencies remained close to historic lows. The 30-day-plus delinquency fee of mortgages ticked up to 2.1{8ba6a1175a1c659bbdaa9a04b06717769bcea92c0fdf198d429188ebbca09471} (purple line in the chart underneath), which was continue to significantly decreased than ahead of the pandemic. For the duration of the Fantastic Moments before Housing Bust 1, in 2005, the delinquency rate was 4.7{8ba6a1175a1c659bbdaa9a04b06717769bcea92c0fdf198d429188ebbca09471}. For the duration of the Good Moments prior to the pandemic, the delinquency level was around 3.5{8ba6a1175a1c659bbdaa9a04b06717769bcea92c0fdf198d429188ebbca09471}.

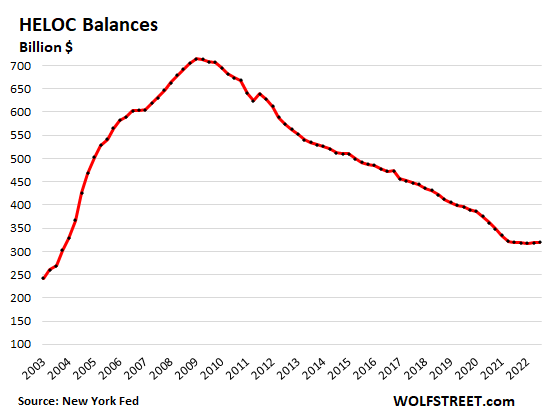

The 30-working day-as well as delinquency rate of HELOCs ticked down to 2.{8ba6a1175a1c659bbdaa9a04b06717769bcea92c0fdf198d429188ebbca09471}. This is right in line with the Fantastic Periods:

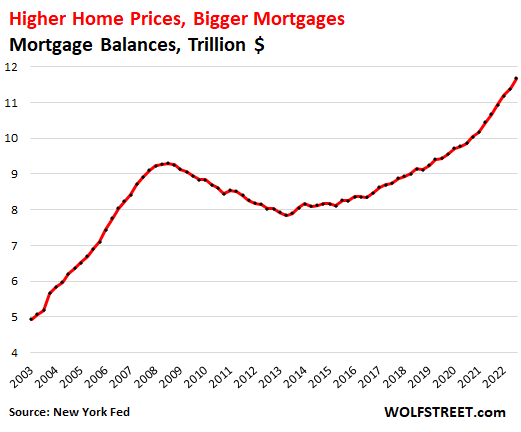

Mortgage loan balances have exploded due to the fact of the exploding home costs in latest decades, even has house sales have plunged in 2022. In Q3, they attained $11.67 trillion:

But HELOC balances experienced been declining at any time due to the fact HELOCs blew up throughout Housing Bust 1, and more than the very last calendar year-and-a-half have crept alongside really reduced amounts and have not appear off those stages nonetheless.

I be expecting that HELOC balances will slowly rise heading forward mainly because pulling cash out of home equity through a dollars-out refi is extremely costly now as the entire home finance loan would appear with existing house loan charges, not just the additional hard cash-out part.

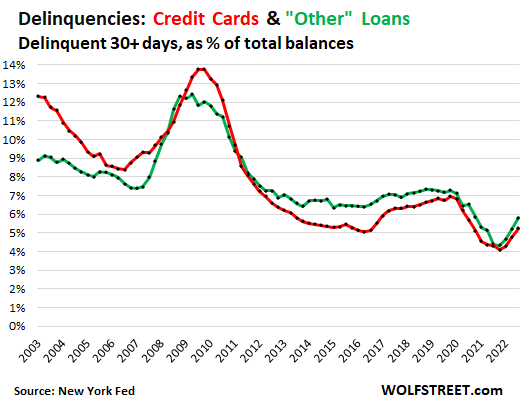

Credit rating cards and particular loans: I mentioned credit rating card balances and delinquencies in considerably detail in this article. The 30-working day-as well as credit-card delinquency rate in Q3 rose to the pre-pandemic minimal of 5.2{8ba6a1175a1c659bbdaa9a04b06717769bcea92c0fdf198d429188ebbca09471} of overall balances (purple line). The delinquency level of “other” client financial loans, this sort of as personalized financial loans, rose to 5.8{8ba6a1175a1c659bbdaa9a04b06717769bcea92c0fdf198d429188ebbca09471} and continues to be perfectly beneath the pre-pandemic lows (eco-friendly line):

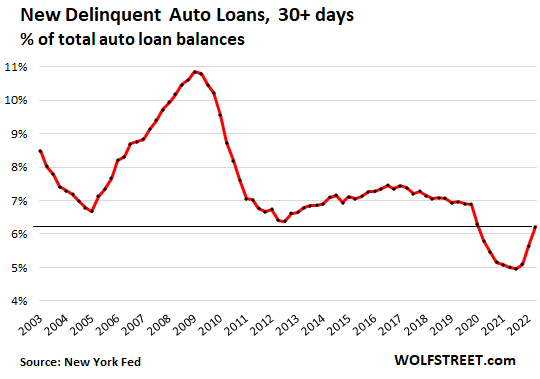

Auto financial loans: I mentioned prime and subprime vehicle loans & delinquencies in depth listed here. The 30-day-as well as delinquency level rose to 6.2{8ba6a1175a1c659bbdaa9a04b06717769bcea92c0fdf198d429188ebbca09471}, still beneath the document lows in advance of the pandemic.

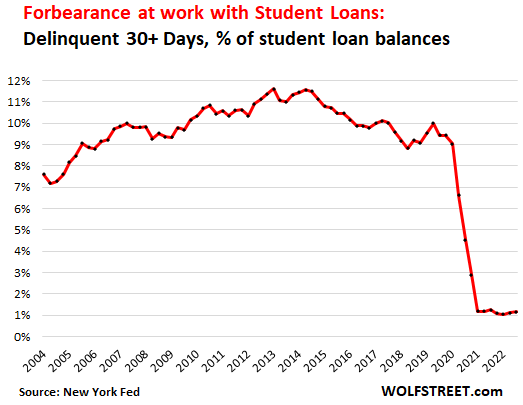

Student financial loan delinquencies are no lengthier delinquencies, and pupil financial loans are nearly no more time financial loans, as significantly as federal student loans are involved, simply because no a person is creating payments on them, and all the things is however on hold, and balances never accrue desire, which has just been extended even further into mid-2023, and partial loan forgiveness has been promised but turns out to be challenging to deliver as a struggle in the courts has ensued.

The only student loans that are delinquent are these held by non-public loan providers, and the general delinquency rate – variety of an absurd notion with student “loans” these days – has plunged:

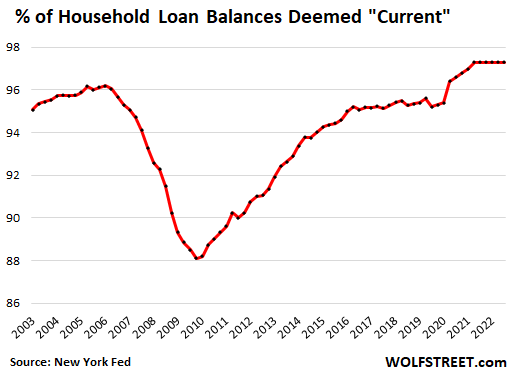

To part of residence bank loan balances deemed “current” (not delinquent) attained a report large in Q2 2021 of 97.3{8ba6a1175a1c659bbdaa9a04b06717769bcea92c0fdf198d429188ebbca09471} of full house bank loan balances, and has remained at this report significant ever since, including in Q3 2022.

These are the overall personal loan balances from all kinds of financial loans – mortgages, car loans, pupil loans, credit rating card balances, and other consumer financial loans – that are “current,” as a per cent of complete mortgage balances excellent:

The Fed has currently reported that the customer can choose more tightening mainly because purchaser equilibrium sheets are in fantastic condition – Powell mentions this at each and every press convention – and mortgage distress is minimal and under historic lows. What individuals can not just take for extended is raging inflation.

Enjoy studying WOLF Road and want to aid it? You can donate. I take pleasure in it immensely. Click on on the beer and iced-tea mug to discover out how:

Would you like to be notified via e-mail when WOLF Avenue publishes a new short article? Sign up below.

![]()

Shareholders Will Want The ROCE Trajectory To Continue")